Insurance is a fundamental part of financial planning, offering a safety net for individuals, families, and businesses. Whether it’s health, car, home, life, or business insurance, understanding how insurance policies work is key to making informed decisions. This guide will walk you through the essential aspects of insurance coverage, its benefits, and the claims process.

What Is an Insurance Policy?

An insurance policy is a legally binding contract between an insurer (the company) and an insured (you). In exchange for premium payments, the insurer agrees to compensate the policyholder for specific financial losses covered under the policy, usually due to unforeseen events like accidents, illnesses, or property damage.

Each policy includes the following key elements:

- Premium: The amount you pay (monthly, quarterly, or annually) for the insurance coverage.

- Coverage: The specific protection provided under the policy (e.g., medical expenses, vehicle repair).

- Exclusions: Conditions or circumstances not covered by the policy.

- Deductible: The amount you must pay out of pocket before the insurer covers the rest.

- Policy Limit: The maximum amount the insurer will pay under the policy.

An insurance policy is a legal contract between an individual or entity (the policyholder) and an insurance company (the insurer). This contract outlines the terms and conditions under which the insurer will provide financial compensation for specific losses, damages, or liabilities that occur due to unforeseen events.

At its core, an insurance policy is designed to transfer risk from the insured to the insurer. By paying a regular fee known as a premium, the policyholder ensures that they will receive financial protection if certain events—such as accidents, illnesses, natural disasters, or theft—take place.

Key Components of an Insurance Policy:

- Premium:

The amount the policyholder pays (monthly, quarterly, or annually) to maintain the policy’s active status. Premiums vary based on the type of coverage, risk factors, and the insured’s profile. - Coverage (Insuring Agreement):

This section specifies what is protected under the policy. For example, in a health insurance policy, coverage might include hospitalization, surgeries, and medications. - Policyholder and Insured:

The policyholder is the person who owns the policy, while the insured is the individual whose risk is covered (in many cases, they are the same person). - Beneficiary:

For certain policies like life insurance, a beneficiary is the person designated to receive the insurance benefits in case of the policyholder’s death. - Deductible:

This is the amount the policyholder must pay out of pocket before the insurer begins to pay. For example, if your car insurance has a ₹5,000 deductible and your repair costs ₹20,000, you pay ₹5,000 and the insurer covers the remaining ₹15,000. - Exclusions:

These are specific conditions or situations that are not covered by the policy. It’s essential to read the exclusions section carefully to understand what is not protected. - Policy Limit:

This refers to the maximum amount the insurer will pay under the policy, either per claim or over the policy’s lifetime.

How It Works:

Let’s say you buy a health insurance policy. You pay a premium each year, and in return, the insurer agrees to pay for certain medical expenses as outlined in your policy. If you get hospitalized and the bill falls within the coverage scope, your insurance company will pay for all or part of the costs—depending on the policy terms, deductibles, and limits.

Types of Insurance Coverage

There are many types of insurance, but here are the most common:

Insurance comes in many forms, each designed to protect against specific types of risks and financial losses. Choosing the right type of insurance depends on your lifestyle, business, property, and personal needs. Below are the most common types of insurance coverage you should know about:

1. Health Insurance

Health insurance provides coverage for medical expenses arising from illness, injury, or preventive care. It can help pay for:

- Doctor visits and hospital stays

- Surgeries and emergency care

- Prescription medications

- Diagnostic tests and specialist care

Health policies can be individual, family floater plans, or provided by employers. In some countries, public or government-backed schemes also offer basic coverage.

2. Life Insurance

Life insurance offers financial protection to your loved ones in case of your untimely death. There are two main types:

- Term Life Insurance: Offers coverage for a specific period (e.g., 10, 20, or 30 years). It pays a death benefit if the insured dies during the term.

- Whole Life or Endowment Plans: Provide lifelong coverage and may include a savings or investment component.

This type of insurance is especially important for breadwinners who want to secure their family’s future.

3. Auto/Car Insurance

Car insurance protects vehicle owners from financial loss due to accidents, theft, or damage. Common coverages include:

- Third-Party Liability: Mandatory in most countries; covers injury or damage to other people or their property.

- Comprehensive Coverage: Includes damage to your own vehicle, theft, fire, natural disasters, and more.

- Collision and Personal Accident Cover: Additional features for extra protection.

4. Home Insuranc

Home insurance covers losses or damages to a residential property and its contents. It usually includes:

- Building Structure Coverage: Protection against fire, floods, earthquakes, or structural damage.

- Contents Insurance: Covers valuables like electronics, furniture, and appliances inside the home.

- Liability Coverage: Offers protection if someone is injured on your property.

This is essential for homeowners and even renters who want to protect their belongings.

5. Travel Insurance

Travel insurance safeguards you during domestic or international trips. It typically includes:

- Trip cancellation or interruption coverage

- Lost baggage and passport support

- Emergency medical coverage abroad

- Travel delay and accident coverage

Ideal for frequent travelers or those going abroad for studies, business, or leisure.

6. Business Insurance

Business insurance protects companies from various risks, depending on the industry and operations. Common types include:

- General Liability Insurance

- Commercial Property Insurance

- Workers’ Compensation

- Professional Indemnity or Errors & Omissions (E&O)

- Cybersecurity Insurance

It’s a must-have for any business owner looking to secure assets, employees, and legal liabilities.

7. Disability Insurance

This insurance provides income replacement if you become temporarily or permanently disabled and unable to work. It helps cover:

- Daily living expenses

- Medical bills

- Long-term care if required

Offered by both private insurers and as part of employee benefits in many organizations.

8. Pet Insurance

Pet insurance covers veterinary expenses related to illness, accidents, or even routine wellness visits. Popular among pet owners who want to avoid high vet bills.

Each type of insurance can be tailored based on your needs and risk level. Some policies even offer riders or add-ons to enhance your coverage.

Key Benefits of Insurance

- Financial Protection: Insurance ensures you’re not left bearing the entire financial burden after an unexpected event.

- Peace of Mind: Knowing you’re covered gives you confidence and reduces stress.

- Risk Management: Especially for businesses, insurance is a way to manage operational and financial risk.

- Legal Compliance: Certain insurances, like car and health insurance, are legally required in many places.

- Investment Component: Some life insurance policies include savings or investment elements.

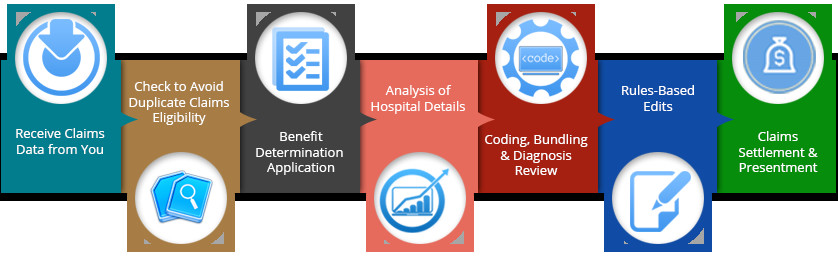

How the Claims Process Works

Filing an insurance claim means you’re asking the insurer to pay for a covered loss. Here’s how the process typically unfolds:

- Notify the Insurer: Contact your insurance company as soon as the incident occurs.

- Submit Documentation: Provide proof of loss, such as photos, receipts, or police reports.

- Assessment: The insurer will evaluate your claim through adjusters or experts.

- Claim Decision: The company will approve or deny the claim based on your policy.

- Payment: If approved, you’ll receive payment up to your policy’s limit, minus any deductible.

Filing an insurance claim can seem intimidating, especially if it’s your first time. But understanding the step-by-step process can help make it smoother and stress-free. Whether you’re claiming for a car accident, hospital bills, or property damage, the basic claims process generally follows the same structure across most insurance types.

Step 1: Notify the Insurance Company

As soon as the incident occurs—whether it’s a medical emergency, accident, or theft—notify your insurance provider. Many companies offer 24/7 customer support through phone, apps, or online portals. Prompt reporting is crucial as delays can impact your claim approval.

Tip: Always note down your policy number and keep emergency contact details handy.

Step 2: Gather and Submit Required Documents

Depending on the type of insurance, you will be asked to submit various documents. Commonly required documents include:

- A filled-out claim form

- Copy of your insurance policy or ID card

- FIR (for theft or accident claims)

- Medical bills and doctor reports (for health insurance)

- Photos or videos of the damage (for property or vehicle insurance)

- Repair bills or invoices

Make sure to provide complete and accurate documentation to avoid unnecessary delays.

Step 3: Claim Assessment or Survey

After receiving your claim, the insurer will assign a claim adjuster or surveyor to evaluate the loss. This could involve:

- Inspecting the damaged property or vehicle

- Interviewing witnesses (for accidents or liability claims)

- Reviewing medical reports and hospital records

- Cross-checking submitted documents

The purpose of this step is to verify the facts and assess the extent of the damage or loss.

Step 4: Approval or Rejection of the Claim

Based on the assessment, the insurer will either:

- Approve the claim (partially or fully), or

- Reject it (if it falls under policy exclusions, fraud suspicion, or insufficient documentation)

You will receive an official communication explaining the decision and, if approved, details on the settlement amount.

Step 5: Claim Settlement

Once approved, the insurance company will process the payment either:

- Directly to you (reimbursement model), or

- To the service provider (cashless model – common in health and motor insurance)

Claim settlements can take a few days to weeks, depending on the complexity of the case and how promptly documents were submitted.

Common Reasons Claims Are Denied

- Filing after the policy’s expiry or lapse

- Claiming for excluded events or damages

- Providing false or incomplete information

- Delay in reporting the claim

- Failure to pay premiums on time

Tips to Ensure a Smooth Claims Process

- Read and understand your policy terms in advance

- Keep all documents organized and handy

- Take pictures or videos as evidence when possible

- Follow up regularly with the insurance company

- Keep a record of all communications

To ensure a smooth claims process, always read your policy carefully and maintain records of all communications and documents.

Final Thoughts

Understanding your insurance policy is crucial in today’s uncertain world. From knowing what’s covered to navigating the claims process, being informed empowers you to choose the right insurance products for your needs. Always compare policies, ask questions, and never hesitate to consult with an insurance advisor for professional guidance.

Also Read: What Does Student Health Insurance Cover And How Does It Work?

Conclusion

Insurance is more than just a contract—it’s a financial safety net that protects you, your family, and your assets from life’s unexpected moments. Whether you’re buying insurance for your car, home, health, or business, understanding your policy’s terms, coverage limits, exclusions, and benefits is essential. A well-chosen insurance policy offers not only peace of mind but also real financial security in the face of uncertainty.

Before committing to any policy, take the time to compare plans, ask questions, and assess your unique needs. With the right information, you can make smarter decisions that safeguard your present and secure your future.

Frequently Asked Questions (FAQs)

What is the difference between a premium and a deductible?

A premium is the amount you pay regularly (monthly, quarterly, or annually) to keep your insurance active. A deductible is the amount you must pay out of pocket before your insurance company covers a claim.

Can I cancel my insurance policy at any time?

Yes, most insurance policies can be canceled at any time. However, you may be charged a cancellation fee, or in some cases, lose out on potential refunds. Always read the cancellation terms in your policy.

What does “policy limit” mean?

The policy limit is the maximum amount an insurer will pay for a covered claim or over the life of the policy. If damages exceed the limit, the extra costs must be paid by the policyholder.

Is it possible to have multiple insurance policies?

Yes. You can hold multiple insurance policies (like health, auto, and home) at the same time. Some policies may even complement each other for broader coverage.

What happens if I miss a premium payment?

Missing a payment can lead to a lapse in coverage. Some insurers offer a grace period, but if payment is not made, your policy may be canceled.

Are all types of losses covered by insurance?

No. Every policy has exclusions—specific risks or scenarios that are not covered. For example, many home insurance policies exclude flood damage unless you purchase additional coverage.